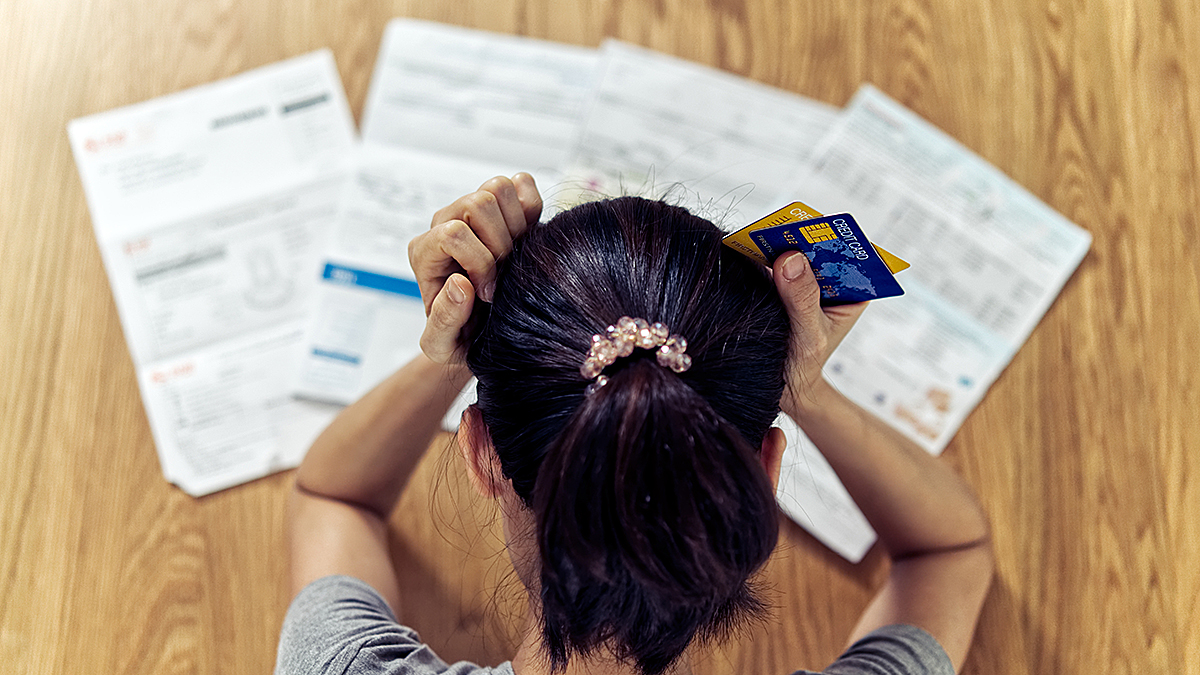

The news story that broke is unequivocal: Canada is on the brink of a debt crisis, and no one seems quite sure what to do about it.

Insolvencies in Canada surged by a third in January compared with a year ago as consumers struggled with rising prices and higher interest rates, the Office of the Superintendent of Bankruptcy said Wednesday.

The federal regulators said there were 9,066 total insolvencies filed in the first month of the year, up 33.7 per cent from 6,779 in January 2022.

As a people person, statistics don’t often raise my pulse. This one was impossible to ignore because of the breadth of scope. “The number of consumer insolvencies for the month rose 33.0 per cent compared with a year earlier.

There were 8,735 insolvency filings by consumers for January, including 1,859 bankruptcies and 6,876 proposals. The result compared with 6,566 insolvency filings by consumers in January 2022 when there were 1,768 bankruptcies and 4,798 proposals.

Meanwhile, business insolvency filings for January were up 55.4 per cent compared with a year ago as they totalled 331, up from 213 in January 2022.”

Andre Bolduc, a licensed insolvency trustee and vice-chairman of the Canadian Association of Insolvency and Restructuring Professionals says, “The impacts of high inflation and numerous interest rate hikes are taking their toll on Canadians.”

“It has been a tough start to 2023 for Canadian businesses,” Bolduc continues. “Many are struggling to manage the impact of higher interest rates, inflation and the continuing effects of the pandemic.”

In spite of the warnings and despite their unpaid bills, consumers are still buying things. That’s a small bright side for your business—for now.

The reality is that half of your Canadian customers are just a day or two’s pay away from having to decide if other creditors’ bills are more important to pay than yours. And of those customers, almost half say they’ll increase their debt to pay their debt in 2023.

When it hits the fan for your customers, many are going to re-prioritize. Your job right now: to position your business to be central among those priorities. Here are 6 ways to do that:

1. Check your data and records.

You have a lot of data. Your accounting software can filter invoices and contracts to identify past-due accounts. Set up a dashboard so you know the moment a payment is past due. If your team doesn’t have a collection process that’s working well, it’s time to start using a good collection agency. An invisible clock starts ticking the moment your customer misses a payment. After 90 days, your outstanding invoice has lost a large chunk of its value; it continues to shrink in value until its collected or expires. Tip: use this Debt Recovery Calculator to see the value of your receivables in real-time.

2. Update Your Contracts

Products change. Warranties change. Laws and regulations change. Make sure your contracts, invoices, and legal paperwork is current and appropriate to the way credit is granted today. I’ve seen companies whose own contracts work against them because they’re out of date or overly simple to offer any real protection or recourses. Technology has made financial transactions so easy that we often rely on the computer to do its job. We assume problems will resolve themselves and AI has got our back. With computers, it’s still garbage in/garbage out. Ineffective or weak contracts are hard to fix once the bills are overdue.

3. Make It Easy To Pay

One thing businesses should do more is talk to their customers. An important thing to discuss is how they prefer to pay their invoices. Mobility has made payments anywhere/anytime payments on the go possible. Few of us carry as much cash as we used to—if even at all. For those rare occasions when a transaction is “cash only,” it’s like saying, “your money is no good here,” because most Canadians’ money is electronic. Hard cash is not only less common, the data reminds us it is in short supply. It’s a little extra work to get multiple payment processes in place, but it’s minor. Payment providers have come a long way in making their services more friction-free for you and your customers. You’ll have made it easier for your customers to make a payment. Reducing payment friction can put you on the “I’ll pay THIS one first” list. The top of the list—or better yet the Paid pile—is where you need to be.

4. Set Shorter Payment Terms

Payment terms vary by industry. Some large-scale manufacturing and resource industries have a universal 90-day payment term as the norm. I’ve submitted invoices and been told payment would be 90 days—or even more. There’s no harm in asking for 30 day payment terms—reasonable and predictable for cash flow. Tell the supplier it’s your policy. You probably aren’t in the business of financing other enterprises—and if you are, it should never be interest-free. And if an existing customer asks for extended terms—consider it very carefully. Extra time is not only a stretch of your resources but one of the warning signs that a business may be in cash trouble.